Google They We have stated which in advance of, it carries repeating: Google medical practitioner home loans and the urban area your local area looking to purchase. Home loan professionals who specialize in handling medical professionals wrote blogs, published about their providers, otherwise has released testimonials of medical professionals, that’ll appear responding towards the browse. See medicalprofessionalhomeloans. This amazing site is actually a catalog and offers a chart out of the united states, and every county provides a trending option. For individuals who just click Washington, a box will come up with title of one’s bank which provides doctor home loans inside Washington, this new contact info to the loan o?cer, and you can a quick general malfunction of bank’s properties and you will program guidance. Th age webpages will not give interest levels.

More 95 per cent of the loans in the usa try already ordered of the Federal national mortgage association, Freddie Mac, otherwise Ginnie Mae, and therefore are old-fashioned, Va, or FHA financing

Regarding best conditions, a doctor home loan will get much more liberal underwriting recommendations, whereas a traditional loan is actually underwritten to a lot more rigid and intransigent assistance. The standard Mortgage As soon as we mention old-fashioned money, we are these are loans that will be purchased because of the Federal national mortgage association and you will Freddie Mac computer. Thus, it doesn’t matter and this bank visit. ) essentially take care of the servicing ones fund, asking monthly, gathering costs, applying escrow accounts, handling taxation and you may insurance, and you will delivering an authored benefits report when the loan should be to be paid off . Th at’s all of the they are doing, oftentimes. Th ey do not indeed individual the mortgage more; https://cashadvanceamerica.net/loans/tribal-loans/ they just get a premium to own repair it. Th e loan is actually built that have a lot of almost every other funds which might be like your personal after which marketed so you can Fannie mae and Freddie Mac, which often bundle all of them and sell all of them because financial-backed securities (ties protected because of the mortgage loans) towards Wall structure Road. Because Fannie and you will Freddie are regulators-sponsored companies, while making loans off coastline-to-coastline, they must provides sweeping, uncompromising recommendations to maintain consistency regarding the style of loans that are brought to them. From inside the doing so, they often provide the lower interest. In acquisition in order to qualify for a traditional loan, your role should suits its rigid guidance just, or match from inside the package, as we call it. Very, a health care professional mortgage isnt a loan that is almost certainly to be released so you’re able to Federal national mortgage association otherwise Freddie Mac computer.

Th age banking institutions (Wells, Chase, Bank from America, etc

The physician Mortgage Generally speaking, a health care provider financial is actually a collection financing tool, meaning that the lender or organization that’s making the financing is simply attending keep the financing and you will keep up with the maintenance of financing. Just like the lender are keeping the mortgage, it makes wisdom contacts underwriting and you will evaluating exposure and you may can also be, hence, take a more liberal means that have physicians than simply it can to have other people, because deems doctors less likely to standard to your loan. Th ere are several regular great things about a doctor financial over a conventional loan: Highest chance of recognition. Medical professionals that have external-the box or tricky points may feel approved to own a physician financial than for a normal financing.

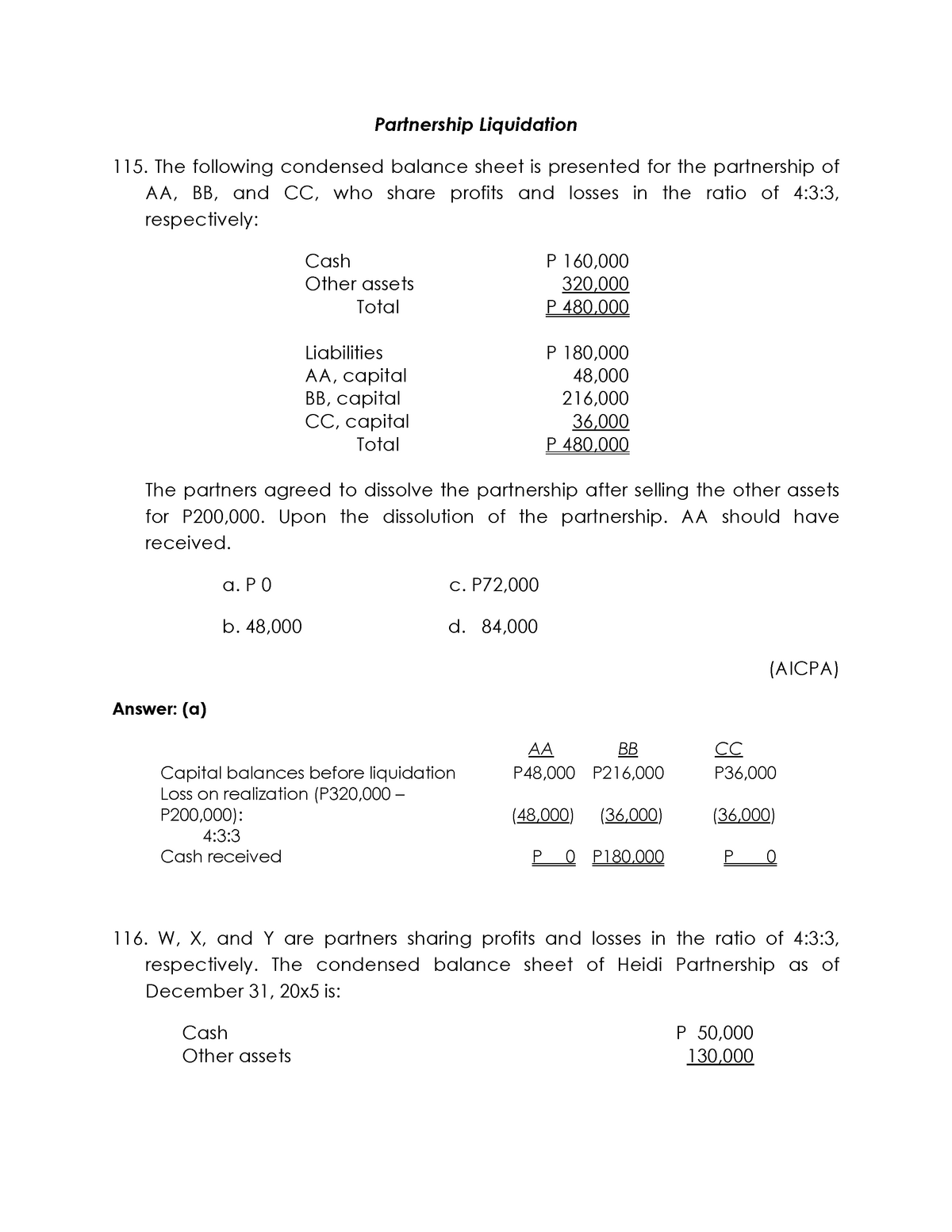

Low down payment. The doctor mortgage often financing large mortgage in order to philosophy, in some instances around 100 per cent of the pick speed. No home loan insurance rates. I’m not sure of every doctor home loan detailed with mortgage insurance policies. Th try is a huge discounts. What if youre to acquire a beneficial $350,000 family and want to lay 5 percent down on good antique mortgage. Dependent on your credit score, in which you reside discovered, and a few other factors, the financial insurance policy is around one percent. To shop for a beneficial $350,000 household setting you’re going to be spending regarding $3,five-hundred a year for the mortgage insurance. More than a decade, that’s $35,000 inside mortgage insurance rates that you’d have to pay that have a normal financing, and you can and this, alternatively, you’d save your self with a physician financial.